Date: 4 May 2026

As the end of financial year (EOFY) approaches in Australia, trustees of self-managed super funds (SMSFs) face one of the most important responsibilities in managing their retirement savings: conducting a thorough SMSF investment strategy review.

This isn’t just a compliance exercise. If it’s done properly, it can significantly improve portfolio outcomes, reduce risk, and ensure your fund is aligned with both regulatory expectations and long-term retirement goals.

With over 1.1 million SMSF members across more than 600,000 funds in Australia, and total assets exceeding $900 billion, SMSFs represent a major part of the superannuation system. Yet, many funds still rely on static or outdated strategies that fail to adapt to changing markets, tax rules, or member circumstances.

In this guide, we’ll walk through how to review your SMSF investment strategy before EOFY, and how to turn that review into a meaningful upgrade in portfolio performance.

Why an SMSF Investment Strategy Review Matters

Under Australian superannuation law, SMSF trustees are required to regularly review their investment strategy. This includes considering:

- Risk and return objectives

- Diversification

- Liquidity needs

- Insurance considerations

- Ability to meet member liabilities

However, in practice, many reviews are treated as a formality – a document signed annually without deeper analysis.

This creates real risks:

- Overconcentration (e.g. too much in property or a handful of shares)

- Unintended risk exposure due to market shifts

- Missed return opportunities from inefficient allocation

- Regulatory scrutiny if the strategy is not genuinely considered

Recent regulatory commentary has increasingly focused on whether SMSF trustees are actively managing risk, not just documenting it.

Download a comprehensive SMSF Investment Strategy Template – auditor ready and defensible.

Step 1: Reassess Your Objectives and Time Horizon

Start with the fundamentals: what is your SMSF trying to achieve?

Key questions to revisit:

- Are members approaching retirement or still accumulating?

- Has income requirement changed?

- Are there new contributions or withdrawals expected?

- Has risk tolerance shifted due to market volatility?

A fund in accumulation phase can generally tolerate more volatility, while a pension-phase fund often prioritises income stability and capital preservation.

Your investment strategy should explicitly reflect these realities, not some assumptions that were valid years ago.

Step 2: Evaluate Current Asset Allocation

Most SMSF performance outcomes are driven primarily by asset allocation, not individual stock picking.

A proper SMSF investment strategy review should assess:

- Allocation across asset classes (equities, fixed income, property, cash, alternatives)

- Domestic vs international exposure

- Growth vs defensive positioning

Common issues seen in SMSFs:

- Heavy bias toward Australian equities

- Significant exposure to direct property

- Under-allocation to international markets

- Excess cash holdings earning low returns

According to industry data, many SMSFs hold over 60% in Australian equities and property combined, creating concentration risk tied to the domestic economy.

A more diversified allocation can improve risk-adjusted returns, especially in volatile markets.

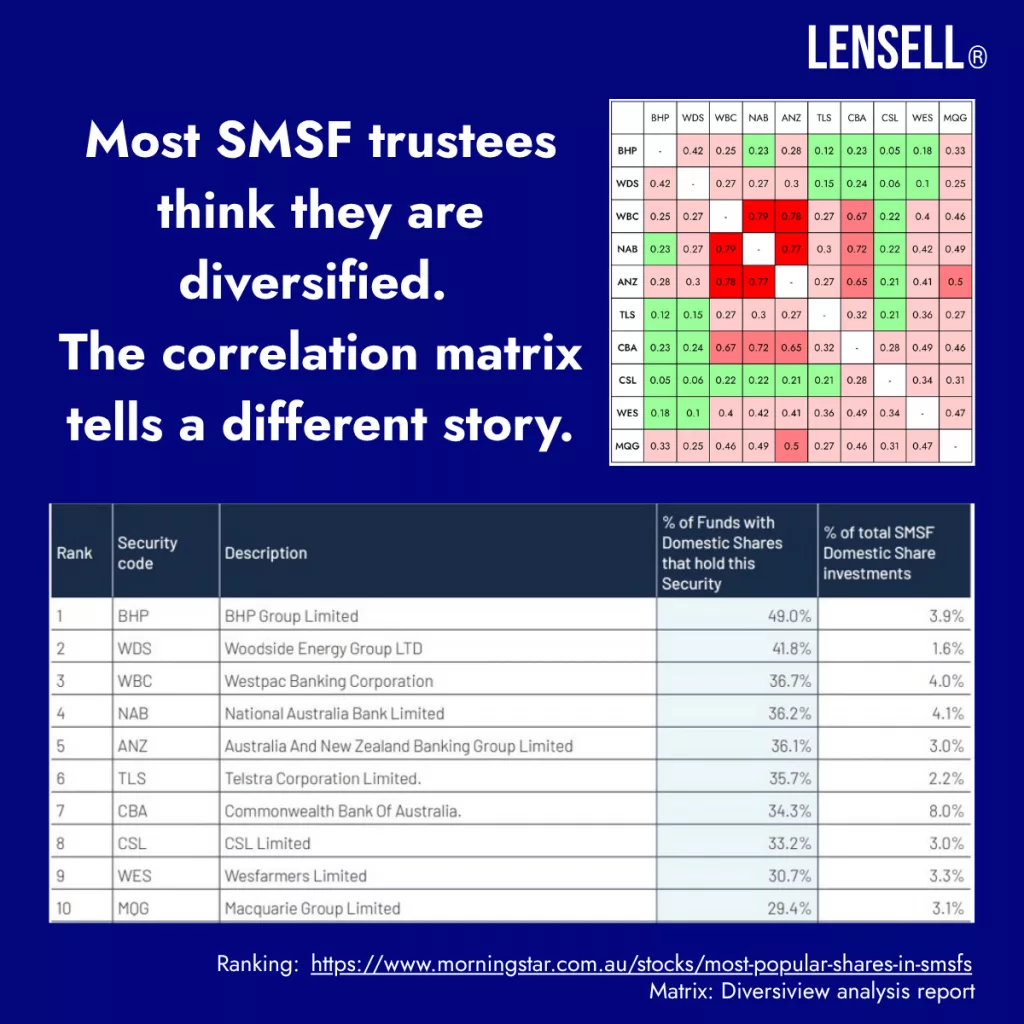

Step 3: Check Diversification (Beyond Asset Classes)

Diversification isn’t just about asset classes, it’s also about:

- Number of holdings and sector exposure

- Correlation between assets

For example, holding 10 Australian bank stocks may appear diversified but is still highly concentrated. See an example below based on the top 10 most popular stocks for SMSF in 2025 (source: https://www.morningstar.com.au/stocks/most-popular-shares-in-smsfs). In this example, there are many positive, strong and very strong positive correlations between stocks, so when one falls, likely a big part of the portfolio will be falling as well.

During your review, consider:

- Are your holdings correlated?

- Do you rely too heavily on a small number of positions?

- Are you exposed to single-sector risks (e.g. financials, mining)?

Modern portfolio tools (such as those used in professional portfolio optimisation, e.g. Diversiview) can quantify this and highlight granular concentration risks.

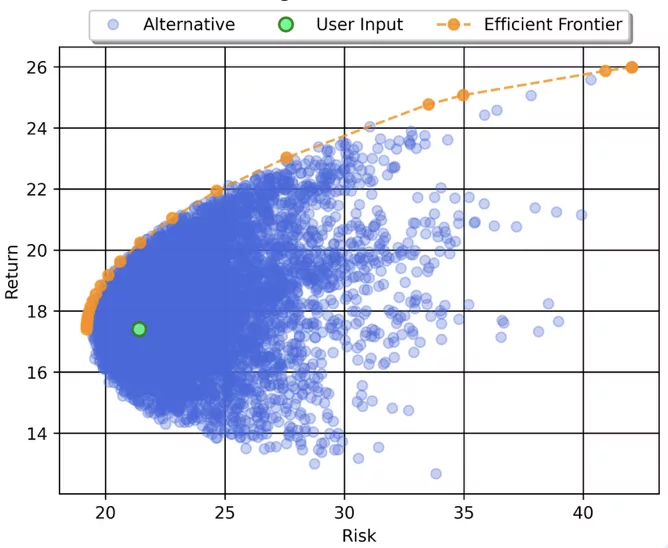

Step 4: Assess Portfolio Risk vs Expected Return

One of the biggest gaps in many SMSF strategies is the lack of quantitative assessment.

Instead of relying on intuition, you should evaluate:

- Expected return (based on historical or modelled data)

- Volatility (risk level)

- Risk-adjusted performance (e.g. Sharpe ratio)

A key question to ask is: Is your portfolio delivering the best possible return for the level of risk you are taking?

Often, the answer is no, meaning the portfolio is inefficient.

This is where optimisation tools like Diversiview can add significant value, by identifying alternative allocations that:

- Improve expected returns

- Reduce risk

- Maintain your investment constraints

An easy, visual way to answer the question above is to look at the Portfolio Universe produced by Diversiview. It shows where the portfolio sits on a risk (X) – expected return (Y) diagram, what other positions are possible, and whether the portfolio is efficient (i.e. on the Efficient Frontier) or not.

Step 5: Review Liquidity and Cash Flow Needs

Liquidity is a critical requirement under SMSF regulations, yet often overlooked.

Your strategy should clearly address:

- Ability to pay pensions

- Expected expenses (tax, fees, insurance)

- Timing of asset sales

Funds heavily invested in illiquid assets (e.g. property) may face challenges meeting obligations without forced sales.

EOFY is the ideal time to check:

- Are you holding sufficient liquid assets?

- Would market downturns impact your ability to pay pensions?

Download a comprehensive SMSF Investment Strategy Template – auditor ready and defensible.

Step 6: Consider Tax Efficiency Before EOFY

EOFY is also a strategic opportunity to optimise tax outcomes within your SMSF.

Key considerations:

- Capital gains vs losses (realisation timing)

- Use of carry-forward losses

- Rebalancing impact on tax position

- Transition between accumulation and pension phase

SMSFs benefit from concessional tax rates, but poor timing of transactions can still erode returns.

A well-planned review ensures your investment decisions align with tax efficiency, not just market views.

Step 7: Rebalance Your Portfolio

Markets move and over time, your portfolio drifts away from its target allocation. Rather than simply rebalancing (selling overweight assets and buying underweight assets), we recommend re-optimisation, where you realign the portfolio with your risk-adjusted returns goal.

EOFY is a natural checkpoint to: review allocations and diversification, lock in gains or losses for tax purposes, maintain portfolio discipline.

Step 8: Ensure Compliance with ATO Expectations

The Australian Taxation Office (ATO) expects SMSF investment strategies to be:

- Documented

- Tailored to the fund

- Regularly reviewed

- Actually implemented

A “generic” or template-based strategy is increasingly viewed as insufficient. Your review should result in:

- Updated documentation

- Clear rationale for asset allocation

- Evidence of consideration of risk, liquidity, and diversification

This is especially important in case of audit.

Step 9: Stress Test Your Portfolio

A sophisticated SMSF investment strategy review goes beyond static analysis. Consider scenarios such as:

- Market downturn (e.g. what if equities go down 20%?)

- Interest rate changes

- Property market decline

- Currency movements

Stress testing helps answer:

- How would your portfolio perform under pressure?

- Can you tolerate potential drawdowns?

- Would your retirement plans still hold?

This is an area where professional-grade analytics can significantly improve decision-making.

Step 10: Identify Opportunities to Improve Outcomes

Finally, your review should lead to action. Look for opportunities to:

- Improve diversification

- Enhance risk-return efficiency

- Introduce new asset classes

- Reduce concentration

- Align more closely with goals

For many SMSFs, even small adjustments in allocation can lead to meaningful improvements in long-term performance.

Common Mistakes to Avoid

When conducting your SMSF investment strategy review, avoid:

- Treating it as a compliance checkbox

- Failing to update strategy despite life changes

- Overconcentration in familiar assets

- Ignoring international diversification

- Making reactive decisions based on short-term market movements

Bringing It All Together

An EOFY SMSF investment strategy review is one of the most valuable exercises a trustee can undertake. It ensures that your fund is:

- Aligned with your retirement objectives

- Properly diversified

- Efficient in its risk-return profile

- Compliant with regulatory expectations

In an environment of market volatility, rising interest rates, and global uncertainty, a static strategy is no longer sufficient.

The most successful SMSFs are those that actively review, analyse, and optimise their portfolios – not just once a year, but as an ongoing discipline.

Conclusion

If your current review process relies on spreadsheets and assumptions, you may be missing key insights. Modern portfolio analytics and technology, including portfolio optimisation, scenario testing, and risk modelling, can provide a clearer, data-driven view of how your SMSF is positioned.

As EOFY approaches, this is the perfect time to move beyond compliance and turn your investment strategy into a true performance driver.

Download a comprehensive SMSF Investment Strategy Template – auditor ready and defensible.

Disclaimer:

LENSELL GROUP Pty Ltd, ACN 646 467 941, trading as LENSELL, is a Corporate Authorised Representative of Foresight Analytics & Ratings Pty Ltd ( Australian Financial Services Licence No. 494552). All information provided to you by LENSELL is intended for general informational purposes only. It does not consider your individual financial circumstances and should not be relied upon without consulting a licensed investment professional or adviser.

The content on this website and in any of its applications is not a financial offer, recommendation, or advice to engage in any transaction. Investment products referenced in our software or marketing literature carry inherent risks, and you should note that past performance does not guarantee any future results. In all our modelling, no transaction costs or management fees are factored into performance analysis.

The information on our website or our mobile application is not intended to be an inducement, offer or solicitation to anyone in any jurisdiction in which LENSELL is not regulated or able to market its services.

Furthermore, all information used across our platform or website may be based on sources deemed reliable but is provided “as is” without guarantees of accuracy or updates. LENSELL and Foresight Analytics & Ratings disclaim all warranties and accepts no liability for any loss or damage resulting from use or reliance on any material or data embedded in our technology platform or digital media. Where liability cannot be excluded by law, it is limited to resupplying the information.

Please view our Financial Services Guide, Terms Of Service and Privacy Policy before making any investment decision using the information available on our website or on any of our applications. LENSELL, Diversiview and StockLenz are trademarks registered in Australia.