Most SMSF trustees know they need an investment strategy. Far fewer know what one actually has to contain, or why their current document might not pass muster if the ATO or their auditor looks closely.

This is not a minor administrative concern.

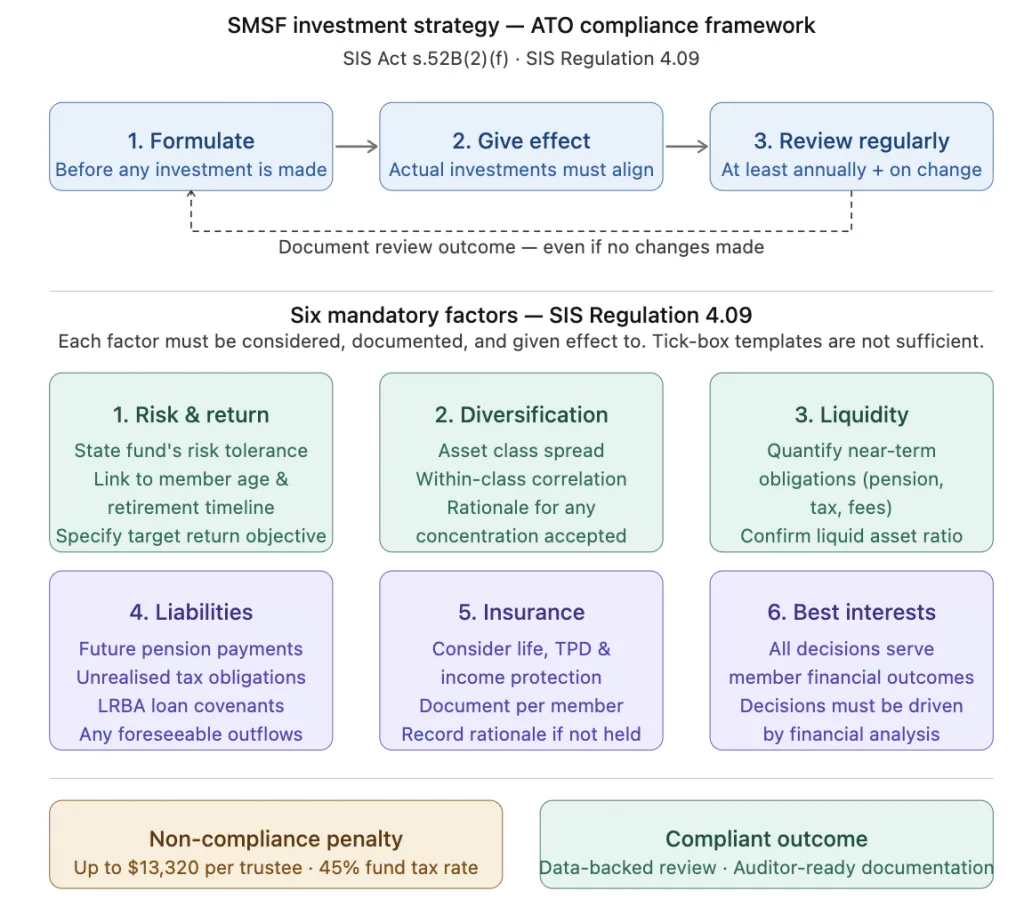

Under the Superannuation Industry (Supervision) Act 1993 (SIS Act), failing to have a properly formulated, implemented, and regularly reviewed investment strategy can result in administrative penalties of up to $13,320 per trustee, potential disqualification as a trustee, and in serious cases, loss of the fund’s complying status – meaning earnings are taxed at 45% rather than 15%.

More importantly, a well-constructed strategy is not just a compliance shield. It is the analytical foundation for a better-performing fund.

This article explains what the ATO actually expects, what your auditor will specifically check, and, critically, what “genuinely considered” means in practice versus on paper.

The Legal Obligation: What the Law Requires

The obligation to have an investment strategy stems from Section 52B(2)(f) of the SIS Act and is given detailed form by Regulation 4.09 of the SIS Regulations. The law requires SMSF trustees to:

- Formulate an investment strategy before making investments

- Give effect to that strategy – meaning your actual investments must align with it

- Regularly review the strategy, and update it when circumstances change

The ATO’s own guidance specifies that trustees should review the strategy at least annually and document that they have done so, including any decisions made during the review — even if the decision is to make no changes.

The strategy must be in writing, tailored to your fund’s specific circumstances, and must not simply repeat the legislation. As the ATO states directly: “It should not be a repeat of the legislation.”

What the ATO Requires You to Consider: The Six Factors

Under SIS Regulation 4.09, your strategy must address six specific factors. These are not optional headings — your auditor is required to verify that each has been considered and documented.

1. Risk and likely return

Your strategy must articulate the fund’s risk tolerance and how it relates to the expected return from investments. This is not a generic statement like “the fund seeks a balance of growth and income.” It should reflect the specific circumstances of each member — their age, proximity to retirement, income needs, and capacity to absorb losses.

A fund with one member aged 62 preparing to draw a pension has a fundamentally different risk profile from a fund with two members aged 40 in accumulation phase. Your strategy should make this explicit.

The ATO does not prescribe what level of risk is acceptable. What it requires is that the level of risk has been consciously chosen and documented, not arrived at by default.

2. Diversification and the risks of inadequate diversification

This is the factor attracting the most regulatory attention in recent years. The ATO has written directly to approximately 17,700 SMSFs identified as holding 90% or more of assets in a single asset or asset class, flagging concerns about concentration risk.

Critically, diversification is not mandated by law — but consideration of it is. A fund concentrated in one asset class is not automatically non-compliant. However, the strategy must document that the trustees have actively considered the diversification question and have a documented rationale for the concentration.

What the ATO and your auditor will look for is evidence that you have thought through:

- How assets are spread across classes (equities, property, fixed income, cash)

- Within-class concentration (e.g. holding only Australian bank stocks does not constitute genuine diversification across equities)

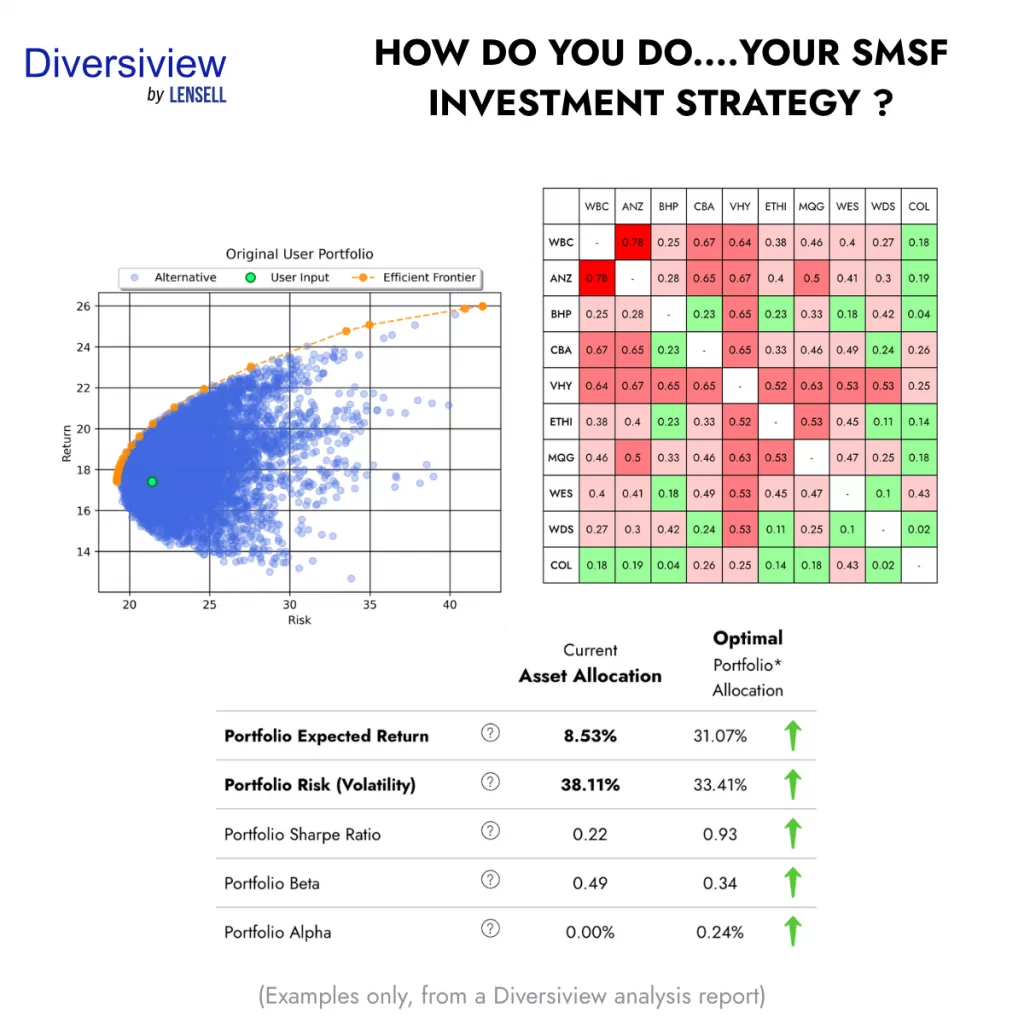

- The correlation between holdings — whether assets tend to move together or independently

This last point is where many SMSF strategies fall short. Asset class diversification is visible and easy to document. Correlation-based diversification requires analytical tools that most trustees do not use.

3. Liquidity

Your strategy must address how easily the fund’s assets can be converted to cash to meet:

- Pension payments to members in retirement phase

- Tax obligations

- Operating expenses (accounting, audit, administration fees)

- Any lump-sum benefit payments

A fund heavily invested in direct property faces a structural liquidity challenge. For example, a property cannot be partially sold to meet a $15,000 pension payment. Your strategy should quantify the fund’s liquidity requirement and confirm that a sufficient proportion of assets is held in liquid form to meet that requirement.

The ATO requires this to be considered, not just noted. A statement that “the fund will maintain sufficient liquidity” without any quantification is unlikely to satisfy a thorough auditor.

4. Ability to discharge existing and prospective liabilities

Related to but distinct from liquidity, this factor requires trustees to consider whether the fund can meet all financial obligations — not just immediate cash needs, but foreseeable obligations including:

- Future pension payments across the expected retirement period of each member

- Potential tax liabilities from unrealised capital gains

- Any borrowing obligations under a limited recourse borrowing arrangement (LRBA)

For funds with LRBAs, asset concentration risk is compounded. A decline in the value of the leveraged asset can both reduce fund value and trigger loan covenant issues simultaneously. The ATO notes this explicitly in its guidance on asset concentration.

5. Insurance

The strategy must document whether the trustees have considered holding life insurance, total and permanent disability (TPD) insurance, or temporary incapacity insurance for each member. Critically, the fund does not have to hold insurance – the obligation is to have considered it and documented the conclusion.

Typical documented rationales include: the member holds adequate insurance through other means (e.g. employment, retail policy); the member is retired and insurance is no longer appropriate; or the cost of insurance within superannuation is disproportionate to the benefit at the member’s age.

A strategy that simply omits the insurance section is non-compliant. A strategy that addresses it (even if just to record a considered decision not to hold insurance) is compliant.

6. The best financial interests of members

Overarching all of the above, every investment decision must be made and documented with reference to the best financial interests of the fund’s members. This is the so-called “best interests duty” that applies to all superannuation trustees. It means investment decisions should be driven by financial analysis and member outcomes, not by personal interest, familiarity with an asset, or external pressure.

What “Genuinely Considered” Means in Practice

The phrase that appears repeatedly in ATO guidance is that trustees must show they have “genuinely considered” each of the six factors above. This is a higher bar than it might appear.

What does not constitute genuine consideration:

- A strategy document that lists the six factors and states the fund “has considered” each, without any fund-specific analysis

- Allocation ranges of 0-100% for each asset class (the ATO has explicitly stated this “is not a valid strategy”)

- A document that has not been updated since the fund was established, regardless of how much circumstances have changed

- A document signed and filed by a trustee who cannot explain what it contains

What does constitute genuine consideration:

- Documented rationale for why the current asset allocation is appropriate for the specific members of the fund at their current life stage

- Explicit acknowledgement of any concentration risk and the reasoning for accepting it

- Quantified liquidity analysis showing the proportion of liquid assets relative to near-term obligations

- Evidence that the strategy has been reviewed, including the date of review, who conducted it, and what was considered, even if no changes were made

Neither the fund’s auditor nor the ATO can review what’s in your head — they need you to write down what you considered

(Heffron SMSF Solutions)

What Your Auditor Will Specifically Check

Every SMSF must be audited annually by a registered SMSF auditor. According to ATO guidance, your auditor is required to verify three things in relation to your investment strategy:

- That an investment strategy exists and addresses the factors in SIS Reg 4.09

- That the fund’s actual investments during the year were consistent with the strategy

- That the strategy was reviewed at some point during the year

If the auditor identifies a breach, they may be required to lodge an Auditor Contravention Report (ACR) with the ATO. The reporting threshold is met if the same breach has occurred in a prior year, or if a prior year breach remains unrectified.

This means a single year of non-compliance may not trigger an ACR, but a repeated failure almost certainly will.

The three most common compliance gaps auditors find:

- Strategy documents that have not been updated to reflect a change in member circumstances (retirement, marriage breakdown, death of a member)

- Investment allocations that materially diverge from the ranges specified in the strategy document

- Strategy documents that address asset class diversification but do not address within-class concentration or asset correlation

The Gap Most Trustees Don’t Know They Have

There is a meaningful difference between what most SMSF strategies document and what a sophisticated assessment of diversification requires.

The standard approach is to document asset class allocations – for example, 60% Australian equities, 20% property, 10% international equities, 10% cash. This satisfies the letter of the diversification requirement at the broadest level.

What it does not address is whether the holdings within those asset classes are genuinely uncorrelated. A portfolio of twelve ASX-listed companies, spread across four sectors, may look diversified. If those companies are all highly sensitive to the same economic conditions (interest rates, commodity prices, the domestic property cycle) they will tend to move together in a market downturn, concentrating risk precisely when diversification is most needed.

Professional portfolio optimisation tools can quantify this at the individual holding level, producing a correlation matrix that shows which pairs of assets tend to move together and which provide genuine diversification benefit. This level of analysis is what distinguishes a defensible strategy (one backed by data) from a generic template.

Turning Compliance Into Performance

A properly conducted strategy review is not just a compliance exercise. It is the most structured opportunity a trustee has to ask: is this portfolio actually positioned to deliver the retirement outcomes we need?

The same analytical process that produces a defensible strategy document – quantifying risk, assessing diversification, modelling expected return, also identifies where the portfolio is inefficient. This means the work done for compliance has direct performance value.

Specifically, a data-driven review can identify:

- Holdings that increase rather than reduce portfolio risk due to high positive correlation with other positions

- Allocation imbalances where the current weights sit away from the efficient frontier — meaning the fund is accepting more risk than necessary for its expected return, or leaving return on the table for the risk it is taking

- Concentration at the individual stock level that is not visible from asset class analysis alone

For SMSF trustees who want to move beyond the compliance minimum, tools like Diversiview calculate the specific weight adjustments that would move a portfolio toward a more efficient position – reducing risk for a given level of expected return, or improving expected return for a given level of risk. The output of this analysis directly supports the documented rationale required by SIS Regulation 4.09.

Ready to create your own SMSF investment strategy? Get our template and start filling it in with your fund specific information.

Disclaimer:

LENSELL GROUP Pty Ltd, ACN 646 467 941, trading as LENSELL, is a Corporate Authorised Representative of Foresight Analytics & Ratings Pty Ltd ( Australian Financial Services Licence No. 494552). All information provided to you by LENSELL is intended for general informational purposes only. It does not consider your individual financial circumstances and should not be relied upon without consulting a licensed investment professional or adviser.

The content on this website and in any of its applications is not a financial offer, recommendation, or advice to engage in any transaction. Investment products referenced in our software or marketing literature carry inherent risks, and you should note that past performance does not guarantee any future results. In all our modelling, no transaction costs or management fees are factored into performance analysis.

The information on our website or our mobile application is not intended to be an inducement, offer or solicitation to anyone in any jurisdiction in which LENSELL is not regulated or able to market its services.

Furthermore, all information used across our platform or website may be based on sources deemed reliable but is provided “as is” without guarantees of accuracy or updates. LENSELL and Foresight Analytics & Ratings disclaim all warranties and accepts no liability for any loss or damage resulting from use or reliance on any material or data embedded in our technology platform or digital media. Where liability cannot be excluded by law, it is limited to resupplying the information.

Please view our Financial Services Guide, Terms Of Service and Privacy Policy before making any investment decision using the information available on our website or on any of our applications. LENSELL, Diversiview and StockLenz are trademarks registered in Australia.